You graduated high school knowing the themes of The Great Gatsby but not how compound interest works on a credit card. That gap is not an accident, and it costs real money.

A 2026 survey found that half of all college students believe their school is not doing enough to make them financially literate. US student loan debt has crossed $1.75 trillion across nearly 43 million borrowers. The money decisions you make between 18 and 22 around budgeting, credit, debt, and investing shape your financial life for the decade that follows.

This guide covers the financial literacy skills every college student needs right now, step by step, starting with the basics and building up to the things most people only learn after making expensive mistakes.

Why Financial Literacy Matters More Than Ever in 2026

The average cost of attending a US college is now $38,270 per year. Gen Z is the least financially confident generation on record, more than one in four say they don’t feel sure about their money knowledge or skills. Only 30% of US adults can cover a $1,000 emergency from savings. That figure includes people with degrees who simply were never taught to handle money before they had to.

Financial literacy is not about being wealthy. It’s about understanding how money works well enough to make decisions that don’t follow you into your 30s. The good news: every skill in this guide is learnable, and the best time to start is before you graduate.

Step 1: Build a Budget That Actually Works

A budget is a spending plan, not a restriction. The goal is to understand where your money comes from: wages, family contributions, financial aid, scholarships and where it goes: tuition, rent, food, transport, subscriptions. Once you can see both sides clearly, you stay in control instead of just guessing.

The most practical framework for students is the 50/30/20 split: 50% of income toward needs, 30% toward wants, and 20% toward savings or debt. If that feels out of reach on a student’s income, start with any intentional split at all. Apps like YNAB, Mint, or the built-in tools inside most bank accounts will track your spending automatically so you’re not logging every transaction by hand.

One habit that delivers outsized results: a ten-minute spending review once a week. You’ll catch forgotten subscriptions, identify patterns before they become problems, and adjust in real time rather than discovering the damage at month’s end.

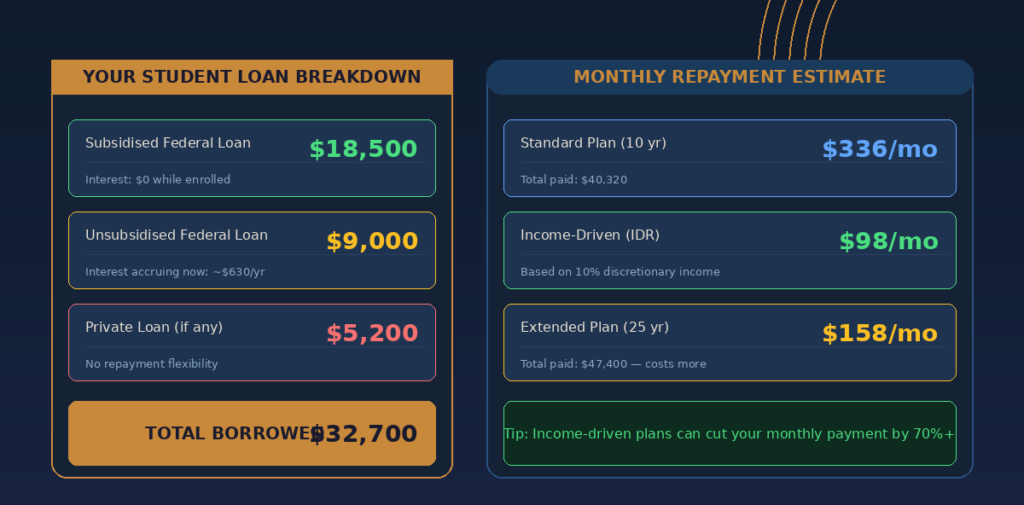

Step 2: Understand Your Student Loans Before You Graduate

Most students sign loan paperwork without reading it. That’s understandable, you’re 18, you need the funding, and the documents are dense. But those terms will follow you for years.

Know the difference between federal and private loans. Federal student loans come with income-driven repayment plans and, in some cases, loan forgiveness options. Private loans don’t. Know whether your loans are subsidised (the government covers interest while you’re enrolled) or unsubsidised (interest accumulates from day one). According to the Federal Student Aid office, income-driven repayment plans can cap monthly payments at 10% of your discretionary income after graduation. Knowing your options before you need them is the entire point.

Run a simple calculation now: take your projected loan balance at graduation and use any free loan repayment calculator to see what your monthly obligation will look like. It won’t take ten minutes, and it’s one of the most clarifying things you can do.

Step 3: Build Your Credit Score the Smart Way

Your credit score is a three-digit number between 300 and 850 that tells lenders how reliably you pay back debt. It affects your ability to rent an apartment, finance a car, or qualify for a mortgage years from now. The earlier you start, the stronger your position in your mid-20s.

The most practical entry point is a secured credit card or a student credit card with a low limit. Use it for one or two regular monthly purchases, groceries, a streaming service and pay the full balance before the due date every month. The two behaviours that matter most are payment history (always on time) and credit utilisation (keep the balance below 30% of your limit).

Avoid the minimum payment trap. A $1,000 balance on a card charging 24% APR, paid down by minimum payments only, can take years to clear and costs far more than $1,000 in total. According to the Consumer Financial Protection Bureau, consistently paying more than the minimum is one of the fastest legal ways to reduce interest costs.

Step 4: Start an Emergency Fund, Even a Small One

An emergency fund is money set aside for unplanned expenses: a medical bill, a broken laptop, a last-minute flight home. The standard guideline is three to six months of expenses on a student’s income, which is a long-term project. Start with a target of $500.

Even a small buffer changes your relationship with unexpected costs. Without one, a $300 emergency means credit card debt. With one, it means a straightforward withdrawal. Keep the fund in a separate savings account, not your everyday checking account, so it’s accessible but not in your daily spending view.

Set up an automatic transfer of $20 or $30 per pay cycle. After a year, you’ll have several hundred dollars earning a small amount of interest and waiting for exactly the moment you need it.

Step 5: Learn the Tax Basics Before Filing Season Arrives

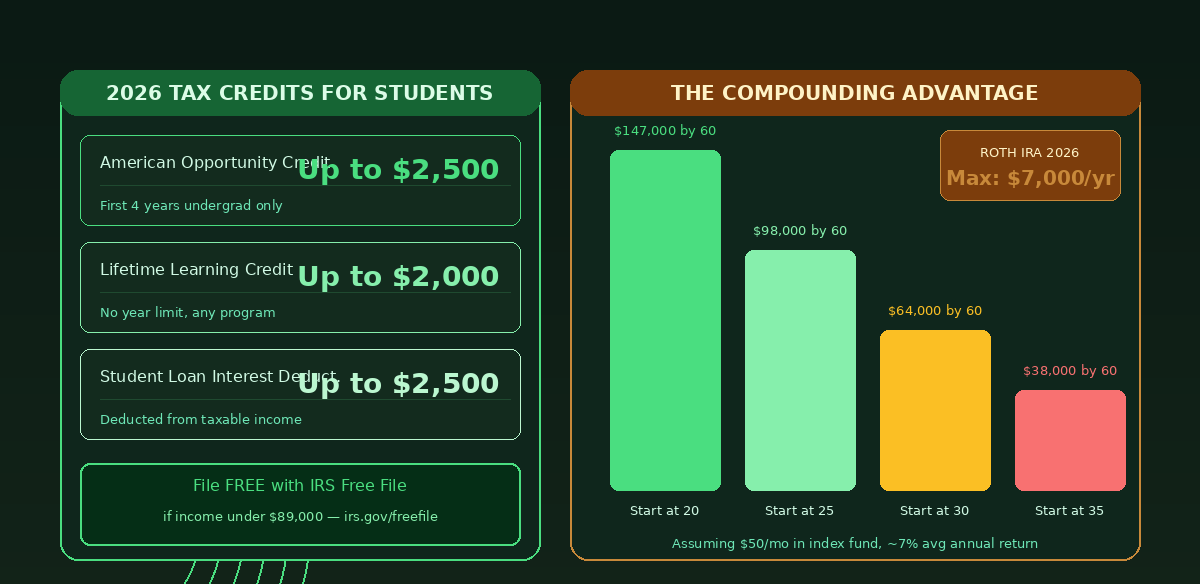

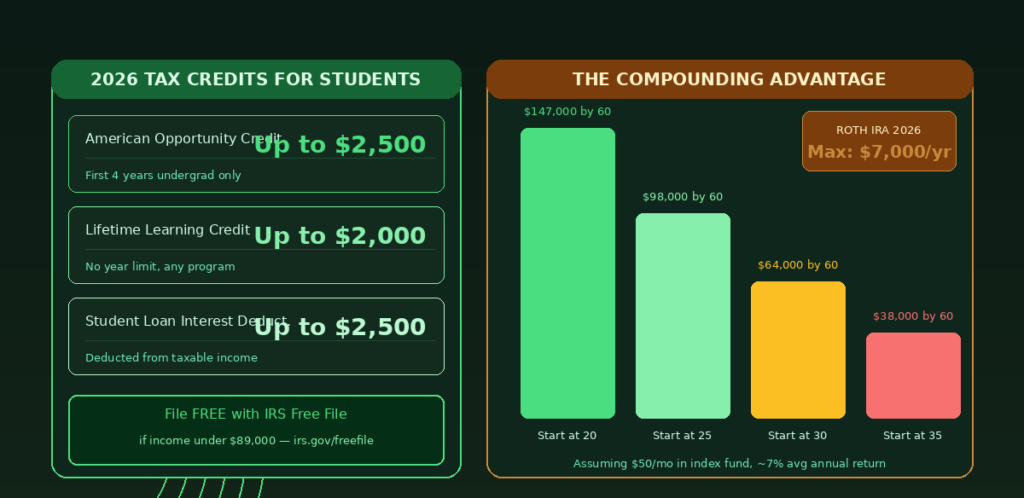

Many college students either don’t file taxes at all or leave money on the table because they don’t know what they’re entitled to claim. In 2026, students who earned more than $15,750 in 2025 must file a federal return. Those who earned less can still file to reclaim taxes withheld from their paychecks.

Two credits are particularly valuable. The American Opportunity Tax Credit (AOTC) provides up to $2,500 per eligible student for qualified education expenses during the first four years of undergraduate study. The Lifetime Learning Credit offers up to $2,000 with fewer eligibility restrictions and no limit on the number of years you can claim it. Students who took out loans can also deduct up to $2,500 in student loan interest paid during the year.

If your adjusted gross income was $89,000 or less, you can file your federal taxes entirely free through IRS Free File. There is no reason to pay for basic tax preparation as a student.

Step 6: Start Investing Early, Even With Very Little

Investing feels like something you do after you have real money. That instinct is expensive. The reason to start early isn’t the amount of time. Compound growth means the money you invest at 20 works much harder than the same money invested at 30, because it has a decade more time to grow.

According to a 2026 WalletHub survey, 66% of Gen Zers believe savings accounts are the best place to put money, compared to 38% of Millennials who prefer stocks. Savings accounts are safe but slow. For long-term goals, retirement, a house deposit, and a low-cost index fund through a Roth IRA are worth understanding now.

A Roth IRA lets you invest after-tax income that then grows tax-free. Contributions in 2026 are capped at $7,000 per year. You don’t need anywhere near that to start. Even $25 per month in a low-cost index fund gives you a base and, more importantly, the habit.

SUMMARY TABLE

Quick-reference: 6 steps to financial literacy in college

| Step | Action | Est. Time to Start |

|---|---|---|

| 1 | Build a monthly budget with a 50/30/20 split | 30 minutes |

| 2 | Review your loan terms and run a repayment estimate | 20 minutes |

| 3 | Open a student credit card; pay in full each month | 15 minutes |

| 4 | Open a separate savings account; auto-transfer $20/month | 10 minutes |

| 5 | Check your tax credit eligibility before filing | 20 minutes |

| 6 | Open a Roth IRA account; contribute any amount | 30 minutes |

VERDICT

Financial literacy for college students comes down to six habits: budget before you spend, understand what you’ve borrowed, build credit deliberately, save a small buffer, file your taxes properly, and start investing early. None of these require a finance degree or a high income. They require time, attention, and a willingness to learn the rules before the stakes get higher.

The students who leave college in the best financial shape are rarely the ones who earned the most. They’re the ones who knew the basics and acted on them early. Start with one step from this guide this week, even just opening a separate savings account and build from there.

FAQ

What is the most important financial skill for a college student?

Budgeting is the foundation. Without knowing how much you’re spending versus earning, every other financial decision happens in the dark. A simple monthly budget, even a rough one, gives you the awareness to make better choices in every other area, from avoiding credit card debt to deciding how much you can save each month.

How do I start building credit with no credit history?

A secured credit card or a student credit card with a low credit limit is the standard entry point. Use it for one or two small recurring purchases each month and pay the full balance before the due date. After six to twelve months of consistent on-time payments, your credit score will begin to establish itself. Avoid applying for multiple cards at once, as each application triggers a hard inquiry that can temporarily lower your score.

Is it worth investing as a college student with very little money?

Yes, because time matters more than the amount. Even $25 per month in a Roth IRA invested in a low-cost index fund gives compound growth a decade more runway than the same contribution started at 30. The habit and the account structure matter as much as the balance when you’re just starting out.

What tax credits can college students claim in 2026?

Two main credits apply. The American Opportunity Tax Credit covers up to $2,500 in qualified education expenses for the first four years of undergraduate study. The Lifetime Learning Credit offers up to $2,000 with no year limit and fewer restrictions. Students who paid student loan interest can also deduct up to $2,500 of that interest from their taxable income. If your income is under $89,000, IRS Free File lets you claim all of this at no cost.

How much should I have in an emergency fund while in college?

A starter target of $500 is realistic and impactful on a student income. It won’t cover everything, but it changes how you handle an unexpected expense from automatic credit card debt to a manageable withdrawal. Once you hit $500, push toward one month of essential expenses. Keep it in a separate savings account so it doesn’t accidentally get spent on everyday costs.

RELATED POSTS

- Best Scholarships for International Students in 2026

- How to Apply for a Student Visa in the UK: Step-by-Step Guide

- Culinary Schools Abroad 2026: Best Programs in Italy, France and Japan